International Journal of Pharmaceutical and Phytopharmacological Research

ISSN (Print): 2250-1029

ISSN (Online): 2249-6084

The importance of risk management in the pharmaceutical industry of any country shows the capability of that country in the field of providing health and the health of that society. The aim of this article is to provide a comprehensive risk management model in the pharmaceutical industry. In this research, an attempt was made to collect the data practically, through a survey method, after receiving the opinions of senior industry experts, and experts familiar with this industry through a researcher-made questionnaire, after confirming the validity and reliability of that data, and then the types of risk. Financial and non-financial risks in the pharmaceutical industry were identified and a comprehensive risk management model was presented using PLS software. To evaluate the confirmatory factor analysis model, the very important index of the square root of the estimation error variance (SRMR) has been used. For this model, the value of this index is equal to 0.079, which can be said that the model has a good fit. This pattern shows that non-financial risks are more effective than financial risks in the pharmaceutical industry. Among the following non-financial risk indicators, operational risk with a path coefficient of 0.970 has the most effect, followed by management risk with a path coefficient of 0.896, and then country risk with a path coefficient of 0.818, and legal risk with a path coefficient of 0.765 is the last influential indicator. Among the following financial risk indicators, market risk with a path coefficient of 0.969 is the most effective, followed by liquidity risk with a path coefficient of 0.855, and credit risk with a path coefficient of 0.769 is the last effective indicator.

INTRODUCTION

The issue of risk management in the pharmaceutical industry was first raised by the US Food and Drug Administration in 2002 under the title of an approach that manages risk. Analyzing the risks in the pharmaceutical industry requires knowing the characteristics of this industry. Extensive changes in the structure of the pharmaceutical products industry (the future-oriented nature of the industry) and the high cost of research and development activities in this industry can be counted among its characteristics. Today, the pharmaceutical industry is progressing along with structural changes. The measurable potential loss of an investment is called risk. Risk is anything that threatens the assets or earning power of the company, institution, or organization in the present or future [1-4].

Integrated risk management has assumed the task of controlling risks and by providing new solutions and innovative strategies, it can create systematic methods for manufacturing, commercial, and service companies. Therefore, the goal of risk management is not to remove risk, but to create an optimal balance between risks and return [5, 6].

Risk in the word means the possibility of danger or facing the risk of injury, loss, loss of income, and loss, and its origin is from the Italian word Riscare, which means to Venture. This concept means taking risks in making a conscious decision [7-9]. However, risk management mainly deals with reducing the adverse effects of internal and external events that adversely affect the organization's activities. Risk management should consist of a set of continuous and developing processes that are used throughout the strategy of an organization and should take into account all the risks related to the past, present, and future systematically. Risk management is the use of financial engineering technology to classify all types of financial assets to control the risk associated with different conditions and situations. These risks include market risk, credit risk, pattern risk, legal risk, and other financial risks [10, 11].

Ramli et al. [12] in research titled "Determining the capital structure and financial performance of the company with the least squares structural equation model approach, evidence from Malaysia and Indonesia" showed that the capital structure with growth opportunities, non-debt tax shield, liquidity, and rate Interest indirectly affects the performance of the company through the leverage of the company, and the coefficients of the effect of these factors are significantly different in Malaysia and Indonesia.

Gadzo et al. [13] in a research entitled "The effect of credit risk and operational risk on the financial performance of global banks in Ghana with the least squares structural equation model approach" revealed that credit risk hurts financial performance. Also, this study showed that bank-specific variables such as asset quality, cost-to-income ratio, banking leverage, and liquidity significantly have a positive effect on operational and credit risk as well as the financial performance of global banks in Ghana.

Avkiran [14] modeled the systematic risk of banks in research entitled "Measuring the systemic risk of Japanese regional banks using partial least squares structural equation modeling". The results of this research showed that the systemic risk of 12.5% is represented by shadow banking.

Seetharaman et al. [15] in an experimental study conducted to calclute the effect of various types of risk on the performance management of credit rating centers, examined different types of risks including market, operational, financial, trade, and credit risks. In addition to identifying important variables, this study focused on establishing a structural framework for future study. Five independent variables were statistically tested by the structural equation model. The findings indicate that credit risk, financial risk, and market risk have a significant effect on the performance of institutions, while business risk and operational risk, although important, do not have a significant effect.

One of the main motivations for increasing interest in financial modeling is the uncertainty about the variables that are proposed in a financial model. Today, more and more companies use financial modeling to manage risk. Risk can be divided into two categories, non-financial risk and financial risk. Risks such as exchange rate risk, credit risk, interest rate risk, and liquidity risk are considered among financial risks, and on the other hand, political risk, industry risk, management risk, and the risk of laws and regulations are considered among non-financial risks [16-18]. The basic question in this research and what is analyzed and studied is what should be the model of comprehensive risk management in the pharmaceutical industry?

MATERIALS AND METHODS

The present research is quantitative. According to the purpose, this study is of the type of applied studies, and in terms of the method of data collection and analysis, it is of descriptive and survey type.

In the current research, a questionnaire was used to collect data, which was made by the researcher and based on theoretical and experimental studies about the variables of the research.

According to the results of the analysis of Cronbach's alpha reliability coefficients, since the reliability coefficients of the research tool are in the range of at least 0.711 to 0.966, it can be said that the tool has a suitable reliability feature.

The statistical population of this research are academic experts in the field of finance who are familiar with the pharmaceutical industry and are senior experts in the pharmaceutical industry. Out of the 50 questionnaires that were distributed, 38 questionnaires were completed and analyzed.

In this research, an attempt was made to collect the data practically, through a survey method, after receiving the opinions of senior industry experts, and experts familiar with this industry through a researcher-made questionnaire, after confirming the validity and reliability of that data, and then the types of risk. Financial and non-financial risks in the pharmaceutical industry were identified and a comprehensive risk management model was presented using PLS software. To evaluate the confirmatory factor analysis model, the very important index of the square root of the estimate of the variance of the error of approximation (SRMR) has been used.

RESULTS AND DISCUSSION

Analysis of research findings

The results of this research are presented in two descriptive and inferential sections. Descriptive statistics (frequency and percentage) are provided. In the inferential part, due to the small size of the sample (multiple indicators of the questionnaire), the PLS (partial least squares) method was utilized with the help of SMARTPLS version 3 software. The method of PLS estimation determines the coefficients in such a way that the resulting model has the greatest power of interpretation and explanation; this means that the model can determine the final dependent variable with the highest precision and accuracy. The method of partial least squares, which is also known as PLS in the discussion of regression modeling, is one of the multivariate statistical methods that can be used despite some limitations, such as the unknown distribution of the response variable, and the presence of a small number of observations. The existence of serious autocorrelation between explanatory variables, one or more response variables modeled simultaneously for several explanatory variables.

Descriptive statistics of demographic variables

The descriptive results of the respondents' demographic characteristics are provided in Table 1.

Table 1. Descriptive results of respondents' demographic characteristics.

|

Variable |

Gender |

Age |

Job position |

Work experience |

|||||||||||

|

Group |

Female |

Male |

30-40 |

40-50 |

>50 |

Expert |

Coach |

Assistant Professor |

Associate Professor |

Professor |

10-15 |

15-20 |

20-25 |

>25 |

|

|

N |

17 |

21 |

6 |

15 |

17 |

25 |

2 |

8 |

2 |

1 |

17 |

10 |

8 |

3 |

|

|

% |

45% |

55% |

16% |

39% |

45% |

66% |

5% |

21% |

5% |

3% |

45% |

26% |

21% |

8% |

|

Inferential analysis of research findings

It is essential to ensure the accuracy of the measurement models of the model variables. This work has been done through multiple confirmatory factor analyses. Confirmatory factor analysis is one of the oldest statistical methods that is used to study the relationship between underlying variables (main variables) and observed variables (questionnaire items) and represents the measurement model. To find out the underlying variables of a phenomenon or summarize the data set, the factor analysis method is used. Factor analysis has two types: confirmatory factor analysis and exploratory factor analysis. In analysis of exploratory factor, the researcher tries to detect the underlying structure of a relatively large set of variables, and the basic assumption is that each variable may be related to each factor. Indeed, the researcher does not have any initial theory in this apporach. In analysis of confirmatory factor, the basic assumption is that each factor is related to a particular subset of variables. The minimum essential condition for confirmatory factor analysis is that the researcher has a specified presupposition about the number of factors in the model before performing the analysis, but at the same time factor analysis is the absence of strong collinearity between the model indicators. The VIF index (Variance Inflation) has been utilized to check inter-branch collinearity. If the value of this index is less than 4, it can be 4 collinearity between the indicators at a desirable and acceptable level. All indicators have lower VIF values. To analyze the questionnaire structure and discover the constituent factors of each variable, factor loadings have been used. The results of factor loadings are shown in Table 2. The factor load indicates how much of the variance of the indicators is explained by the underlying variable. The value of this index should be greater than 0.5 and significant within the 95% confidence interval. The significance of this index is obtained by Bootstrapping or Jackknifing. An index that has a higher factor load has a higher importance in measuring the corresponding component. All indicators have a factor load greater than 0.5 and a t-statistic value greater than 1.96 (significance level is less than 0.05).

Table 2. Factor loadings.

|

Main variables |

Indicator |

First-order confirmatory factor analysis |

Second-order confirmatory factor analysis |

Collinearity index |

|||

|

Factor load |

T |

P-Value |

Factor load |

T |

|||

|

Credit risk |

FCR1 |

0.818 |

8.829 |

0.000 |

0.769 |

10.158 |

1.432 |

|

FCR2 |

0.815 |

7.594 |

0.000 |

1.558 |

|||

|

FCR3 |

0.754 |

5.587 |

0.000 |

1.296 |

|||

|

Liquidity risk |

FLR1 |

0.784 |

5.575 |

0.000 |

0.855 |

27.484 |

2.007 |

|

FLR2 |

0.823 |

8.855 |

0.000 |

2.149 |

|||

|

FLR3 |

0.826 |

23.700 |

0.000 |

1.255 |

|||

|

Market risk |

FMR1 |

0.864 |

14.998 |

0.000 |

0.969 |

92.776 |

3.604 |

|

FMR2 |

0.878 |

15.465 |

0.000 |

2.277 |

|||

|

FMR3 |

0.887 |

27.435 |

0.000 |

2.792 |

|||

|

FMR4 |

0.842 |

13.834 |

0.000 |

2.619 |

|||

|

FMR5 |

0.854 |

18.083 |

0.000 |

2.119 |

|||

|

FMR6 |

0.890 |

17.012 |

0.000 |

2.487 |

|||

|

FMR7 |

0.906 |

29.342 |

0.000 |

2.321 |

|||

|

Country risk |

NFCR1 |

0.780 |

8.349 |

0.000 |

0.818 |

14.841 |

1.503 |

|

NFCR2 |

0.884 |

13.354 |

0.000 |

1.905 |

|||

|

NFCR3 |

0.727 |

6.223 |

0.000 |

1.367 |

|||

|

Legal risk |

NFLR1 |

0.905 |

17.092 |

0.000 |

0.765 |

10.953 |

2.265 |

|

NFLR2 |

0.874 |

19.593 |

0.000 |

1.792 |

|||

|

NFLR3 |

0.653 |

3.499 |

0.000 |

1.414 |

|||

|

Management risk |

NFMR1 |

0.915 |

31.102 |

0.000 |

0.896 |

20.503 |

3.878 |

|

NFMR2 |

0.898 |

31.282 |

0.000 |

3.961 |

|||

|

NFMR3 |

0.789 |

8.883 |

0.000 |

1.973 |

|||

|

NFMR4 |

0.927 |

41.449 |

0.000 |

3.805 |

|||

|

Operational risk |

NFOR1 |

0.898 |

27.679 |

0.000 |

0.970 |

129.536 |

2.684 |

|

NFOR2 |

0.851 |

15.311 |

0.000 |

3.726 |

|||

|

NFOR3 |

0.869 |

22.293 |

0.000 |

2.497 |

|||

|

NFOR4 |

0.748 |

10.802 |

0.000 |

1.987 |

|||

|

NFOR5 |

0.578 |

3.530 |

0.000 |

1.856 |

|||

|

NFOR6 |

0.740 |

8.116 |

0.000 |

3.748 |

|||

|

NFOR7 |

0.850 |

16.388 |

0.000 |

2.023 |

|||

|

NFOR8 |

0.626 |

4.214 |

0.000 |

1.998 |

|||

One of the convergent validity indicators is the Average Variance Extracted (AVE) index. The average variance extracted is a measure of convergence among a set of observed items of a construct. A percentage of the explained variance is among the items. This average extracted variance should be higher than 0.5 to confirm convergent validity. As can be seen in the above tables, the value of this variable for the model constructs with an average value of the explained variance is higher than 0.5, and it shows the confirmation of convergent validity in the model. Another convergent validity index is the Rho_A index according to Hensler et al. which needs to have a value above 0.6. This index was also higher than the permissible limit for all research variables. To check the reliability of the research variables, two composite reliability indexes and Cronbach's alpha were used. Composite reliability and Cronbach's alpha according to Forner and Larcker should be 0.7 or higher, which indicates sufficient internal convergence. Internal consistency is the reliability that uses both Cronbach's alpha and composite reliability. Both indicators examine internal consistency. For all research variables, combined reliability and Cronbach's alpha value are greater than 0.7, which shows the measurement tool reliability.

Another test to determine the measurement model is its quality check test. The measurement model quality is determined by the sharedness index with cross-validity (Q2). This index measures the path model's ability to predict observable variables through their corresponding latent variable values. If this index reveals a positive number, the measurement model has the necessary quality. To study the entire measurement model, this index average is taken, and if it is positive, the entire measurement model is of good quality. The results of this test are given in Table 3, as you can see, this index is positive for all the variables in the research, and the total average of this index is 0.419, which indicates the high quality of the measurement model.

Table 3. Convergent validity and reliability index.

|

Model variables |

Validity and reliability indicators |

||||

|

Cronbach's alpha |

rho_A |

Composite reliability |

AVE |

Cross-validation |

|

|

Comprehensive risk in the pharmaceutical industry |

0.966 |

0.971 |

0.969 |

0.744 |

0.424 |

|

Financial risk |

0.935 |

0.944 |

0.945 |

0.788 |

0.467 |

|

Non-financial risk |

0.944 |

0.953 |

0.951 |

0.807 |

0.422 |

|

Credit risk |

0.711 |

0.715 |

0.838 |

0.634 |

0.28 |

|

Market risk |

0.949 |

0.949 |

0.958 |

0.765 |

0.64 |

|

Operational risk |

0.903 |

0.921 |

0.923 |

0.605 |

0.452 |

|

Legal risk |

0.756 |

0.825 |

0.856 |

0.669 |

0.35 |

|

Risk management |

0.905 |

0.911 |

0.934 |

0.781 |

0.582 |

|

Liquidity risk |

0.755 |

0.798 |

0.852 |

0.658 |

0.292 |

|

Country risk |

0.713 |

0.721 |

0.841 |

0.639 |

0.282 |

Table 4 reveals the correlation coefficients for check the relationship between the hidden variables two by two. The main diameter of this matrix shows the square root of the average explained variance (AVE root). Based on this index, the variance of each existing variable must be higher for its related indices than for other indices. To detect this, first, the square root of the AVE of the latent variables is determined and then the finding is compared with the correlation values that this latent variable has with other latent variables. It should be the square root of AVE of correlation values. For example, the square root of the average variance explained for the credit risk variable is (0.796), which is higher than the correlation value of this variable with other variables. As it is clear in the table, the value of the square root of the average explained variance index for all variables is greater than the correlation of that variable with other variables.

Table 4. Correlation coefficients and divergent validity index.

|

Hidden Variables |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

|

Credit risk |

0.796 |

|

|

|

|

|

|

|

Market risk |

0.634 |

0.875 |

|

|

|

|

|

|

Operational risk |

0.510 |

0.535 |

0.778 |

|

|

|

|

|

Legal risk |

0.599 |

0.480 |

0.543 |

0.818 |

|

|

|

|

Risk management |

0.590 |

0.598 |

0.517 |

0.502 |

0.884 |

|

|

|

Liquidity risk |

0.594 |

0.755 |

0.633 |

0.585 |

0.665 |

0.811 |

|

|

Country risk |

0.678 |

0.500 |

0.515 |

0.543 |

0.510 |

0.608 |

0.800 |

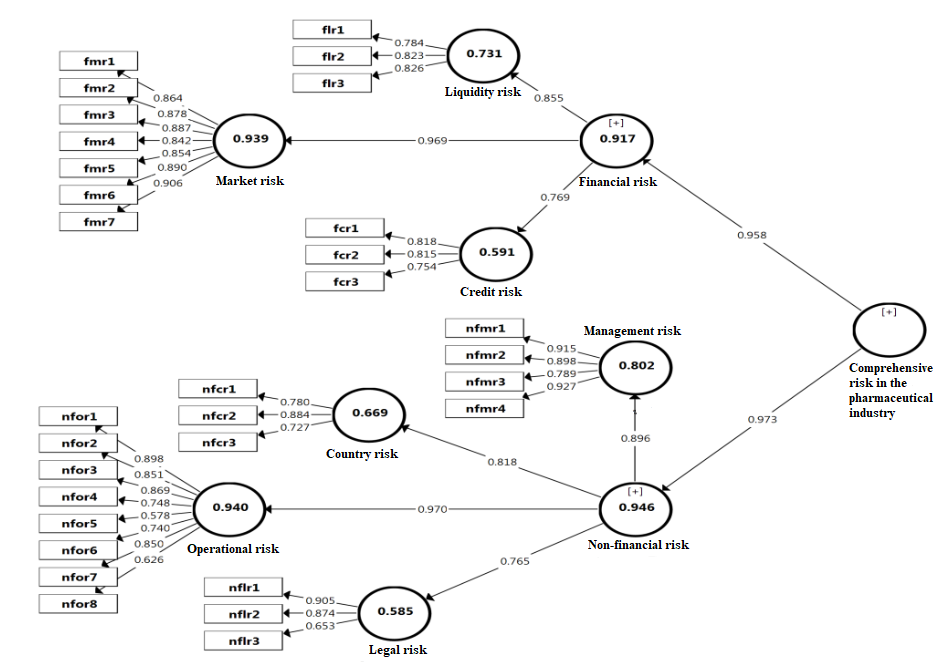

To evaluate the confirmatory factor analysis model (Figure 1), the very important index of the square root of the estimated error variance of approximation (SRMR) has been used. The limit of this index is 0.1. For this model, the value of this index is equal to 0.079, and considering that it is less than 10%, it can be said that the model has a good fit.

|

|

|

Figure 1. The comprehensive risk management model of the pharmaceutical industry (source: research findings). |

Risk management is the process of analyzing, identifying, and responding to risk factors, which includes complex techniques. Environmental uncertainty, intense competition, and flexibility of technology have made organizations and their managers face many challenges. To effectively manage these challenges in the pharmaceutical industry, a comprehensive risk management model has been presented in this research by identifying and analyzing the risks of this industry. The presented model shows that non-financial risks and financial risks have a positive and significant effect. According to these results, it can be said that non-financial risks (operational risk, management risk, legal risk, and country risk) have a greater effect than financial risks (credit risk, liquidity risk, and market risk) and to risk managers in Pharmaceutical companies are suggested to consider non-financial risk first and then financial risk in their decisions. Among the non-financial risk indicators, operational risk has the most effect, followed by management risk, country risk, and legal risk. Among the following indicators of financial risk, market risk is the most effective, followed by liquidity risk and credit risk.

According to the presented model, operational risk in the pharmaceutical industry is considered the most effective non-financial risk. The dimensions affecting it include cyber security risk, quality risk, technology flexibility risk, accident risk, equipment failure risk, design (model) risk, fraud risk, and finally human resource risk. To combat cyber threats using explicit recommendations to facilitate the exchange of information between broad industries in cyber and physical environments, the US Department of Homeland Security has strengthened its National Infrastructure Protection Program on Cybersecurity by issuing Executive Order 13800 (Strengthening cyber security of federal networks and critical infrastructure) to achieve the ultimate goal of these policies, by identifying and prioritizing risks in the operational period [19]. These contents can be an indication of the importance of this risk. The results obtained in this research confirm the importance of cyber risk in the pharmaceutical industry. Low-quality products in the pharmaceutical industry threaten people's lives. Pharmaceutical companies must produce their products with the highest quality so that they can directly affect the health of patients. On the other hand, the failure of any machinery (equipment) of the facility leads to disruptions in the production process of pharmaceutical products, which are operational risk dimensions according to the results obtained. It seems that the risk of human resources is one of the most important operational risks, while in this industry it has been identified as the factor that has the least effect. Perhaps this case can be explained in the way that due to the high level of knowledge of the people who are working in this industry, this risk has shown the least effect in the pharmaceutical industry. According to the obtained results, risk managers in pharmaceutical companies are suggested to increase their competitive advantage in this industry by developing cyber systems, improving product quality, and using up-to-date technologies.

According to the presented model, risk management is effective after operational risk in the pharmaceutical industry. The dimensions affecting it are strategy risk, managers' inexperience risk, outsourcing decision risk, and finally contract decision risk. According to the results obtained in this model, it is suggested that risk managers in pharmaceutical companies, by carefully examining the opportunities and threats to achieve the company's business goals, using experienced and committed managers, handing over some activities that are aimed at They are not the mission of the company, and finally manage the risk management in the company by signing appropriate contracts.

According to the presented model, country risk is the third sub-index of non-financial risks in the pharmaceutical industry. Legal risk is the fourth sub-indicator affecting non-financial risk in the pharmaceutical industry, the dimensions affecting it are monitoring risk, compliance acceptance risk, and reputation risk (record). According to the presented model, market risk is the first sub-index affecting financial risk in the pharmaceutical industry. The dimensions affecting it are execution risk, competitive risk, market-making risk, interest rate risk, exchange rate risk, commodity price risk, and finally market uncertainty risk. It is suggested to the risk managers of the company to get the satisfaction of their shareholders by managing the execution risk. According to the presented model, liquidity risk is the second most effective sub-index of financial risk in the pharmaceutical industry. The dimensions affecting it are company liquidity risk, market liquidity risk, and finally financing liquidity risk. The inability of the company to pay its obligations is called financial risk. This risk is controlled by proper cash flow planning [20-23].

According to the presented model, credit risk is considered the third sub-indicator affecting financial risk in the pharmaceutical industry. The dimensions affecting it are customer credit risk, credit reduction risk, and company credit risk, respectively. Regarding the credit risk of customers, we can mention the risk related to drug insurance due to the high cost of preparing some drugs for manufacturers. It is recommended to risk managers to pay more attention to the credit of their customers so that they do not face pending claims and on the other hand, to increase their credit according to the liquidity situation.

CONCLUSION

The importance of risk management in the pharmaceutical industry of any country shows the capability of that country in the field of providing health and the health of that society. The aim of this article is to provide a comprehensive risk management model in the pharmaceutical industry. To evaluate the confirmatory factor analysis model, the very important index of the square root of the estimation error variance (SRMR) has been used. For this model, the value of this index is equal to 0.079, which can be said that the model has a good fit. This pattern shows that non-financial risks are more effective than financial risks in the pharmaceutical industry. Among the following non-financial risk indicators, operational risk with a path coefficient of 0.970 has the most effect, followed by management risk with a path coefficient of 0.896, and then country risk with a path coefficient of 0.818, and legal risk with a path coefficient of 0.765 is the last influential indicator. Among the following financial risk indicators, market risk with a path coefficient of 0.969 is the most effective, followed by liquidity risk with a path coefficient of 0.855, and credit risk with a path coefficient of 0.769 is the last effective indicator.

Acknowledgments: None

Conflict of interest: None

Financial support: None

Ethics statement: None